- Details

- Category: Windtech Future

Gearboxes are a critical component in a wind turbine, helping to convert rotational energy into electrical power to drive the energy transition across the world. According to the Global Wind Gearbox Supply Chain Update 2019 published by the Global Wind Energy Council (GWEC) Market Intelligence service in December 2019, the market for the gearbox supply chain is set to grow as more wind turbines are installed in new markets for both onshore and offshore wind, and since more renewable energy systems must be installed to decarbonise the global energy system.

Gearboxes are a critical component in a wind turbine, helping to convert rotational energy into electrical power to drive the energy transition across the world. According to the Global Wind Gearbox Supply Chain Update 2019 published by the Global Wind Energy Council (GWEC) Market Intelligence service in December 2019, the market for the gearbox supply chain is set to grow as more wind turbines are installed in new markets for both onshore and offshore wind, and since more renewable energy systems must be installed to decarbonise the global energy system.By Feng Zhao, Strategy Director at Global Wind Energy Council

- Details

- Category: Windtech Future

The global offshore wind energy market appears poised for significant growth in the coming years, driven by demand as well as cost reductions in new technology. IntelStor has previously predicted a global offshore wind market of 355GW by 2050, up significantly from the current levels of ~49GW expected to be installed globally by the end of 2019.

The global offshore wind energy market appears poised for significant growth in the coming years, driven by demand as well as cost reductions in new technology. IntelStor has previously predicted a global offshore wind market of 355GW by 2050, up significantly from the current levels of ~49GW expected to be installed globally by the end of 2019.By Philip Totaro, Founder and CEO, IntelStor, USA

- Details

- Category: Windtech Future

The contribution of digital services to operations and maintenance (opex) cost savings, service revenue enhancement, asset life extension and additional power delivered to the grid in a price optimal fashion has so far fallen short of expectations in the five years since these solutions were first deployed.

The contribution of digital services to operations and maintenance (opex) cost savings, service revenue enhancement, asset life extension and additional power delivered to the grid in a price optimal fashion has so far fallen short of expectations in the five years since these solutions were first deployed.By Philip Totaro, Founder and CEO, IntelStor, USA

- Details

- Category: Windtech Future

Since 1995 the wind energy industry has suffered more than US$ 5.2 billion in commercial losses associated with intellectual property risks which went unmitigated and could have been avoided.

Since 1995 the wind energy industry has suffered more than US$ 5.2 billion in commercial losses associated with intellectual property risks which went unmitigated and could have been avoided.By Philip Totaro, Founder and CEO, IntelStor, USA

- Details

- Category: Windtech Future

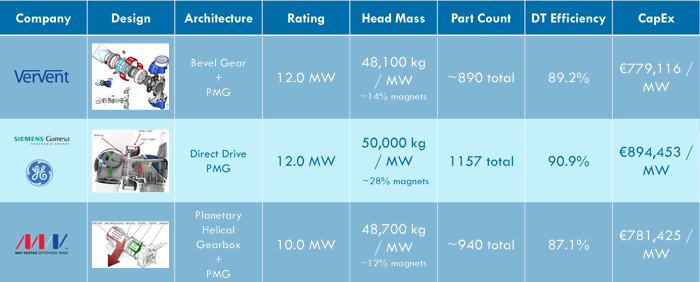

As the wind turbine market enters a new era driven by subsidy-free and tax-credit-free cost parity, a new generation of wind energy technology is poised to hit the market by 2020. Markets which are shifting towards a competitive tendering process continue to drive the need for higher annual energy production as well as lower capex, opex and levelised cost of electricity.

As the wind turbine market enters a new era driven by subsidy-free and tax-credit-free cost parity, a new generation of wind energy technology is poised to hit the market by 2020. Markets which are shifting towards a competitive tendering process continue to drive the need for higher annual energy production as well as lower capex, opex and levelised cost of electricity.By Philip Totaro, Founder and CEO, IntelStor, USA

- Details

- Category: Windtech Future

With more than US$ 647 million of foreign direct investment in offshore wind project development and domestic supply chain ramp-up at stake, Taiwan risks losing its mantle as one of the hottest offshore wind energy markets in the world. At the heart of this is the change in the feed-in tariff, which could face a steep reduction.

With more than US$ 647 million of foreign direct investment in offshore wind project development and domestic supply chain ramp-up at stake, Taiwan risks losing its mantle as one of the hottest offshore wind energy markets in the world. At the heart of this is the change in the feed-in tariff, which could face a steep reduction.By Philip Totaro, Founder and CEO, IntelStor, USA

- OEMs are Shifting Towards Global Supply Chain Cost Optimisation at the Expense of Optimal Turbine Levelised Cost of Energy

- With +10MW Offshore Turbines as the New Normal in Europe, Where Do the Chinese OEMs Go Next?

- Wind LCOE Set to Drop Further Thanks to the Expiration of Seminal Patents

- The Right Product Mix and a Modular Architecture Can Protect OEM Profits in the Age of Tenders

- Renewable Energy Digitalisation Growth Poised to Reap Benefits for the Data Rich

- Turbine OEMs with Product Portfolio Diversity are Most Successful in US Wind Market

- Enercon Acquisition of Lagerwey Enables Competitive Product Evolution with PMG Technology

- Commercial Value of Data Has Increased Thanks to Digitalisation

- Onshore Wind Turbine Tech to Top Out in Ten Years

- Hybrid Materials and 3D Printing Enabling SciFi Wind Turbine Structures

- Can Wireless Mesh Networks Kill Slip-Rings?

- Offshore Wind Yet to See Meaningful Digital Services Deployment

- Focus on TLPs, Predictive Maintenance and AEP Optimisation to Further Reduce Offshore LCOE

- Renewable energy Internet of Things to hit US$ 5.3 billion annually by 2030

- Onerous Mandates on Performance Impact or Reliability are Stifling RE Innovation

- Emergence of Digital Services Highlights Need for Content Licensing Business Model

- Digitalisation Necessitates New Thinking and New Business Models

- How Common Platform Wind Turbine Architecture Unlocks Export Markets

- Closing the Product Competitiveness Gap

- Offshore Innovation Seeing Lift-off

- Consolidation Spurs Wind Innovation Revival

- The future of technology – Services

- Power plant control

- The Rise of Asian Innovation

- The future of technology – Manufacturing

- The future of technology – Materials

Stay informed with Windtech International! Sign up here for our free newsletters

| Turbine Shots

brought to you by

|

|

") |

|

| #25 GE Vernova wind turbines installed at El Mezquite wind farm near Monterrey, Mexico (courtesy Alberto Salinas) | |

| Every week on our website and in our email newsletter we want to show you that wind energy is more than just technology. We therefore invite you to send stunning pictures of wind turbines inspired by “light” (in the broadest sense of the word). After 52 submissions we will announce the winner of the year’s best picture! Email your photo to Include turbine model, location and name of photographer. (size of the published photo will be 336 px width x 280 px high). |

|

|

|

Use of cookies

Windtech International wants to make your visit to our website as pleasant as possible. That is why we place cookies on your computer that remember your preferences. With anonymous information about your site use you also help us to improve the website. Of course we will ask for your permission first. Click Accept to use all functions of the Windtech International website.