When the first floating offshore wind demonstration projects were deployed nearly ten years ago, most observers thought that the technology was intriguing, but the costs and degree of difficulty were both very, very high. At that stage, fixed-bottom offshore was installing only a few hundred megawatts per year, costs were high and going up, and the future of the sector appeared in doubt. How things have changed!

When the first floating offshore wind demonstration projects were deployed nearly ten years ago, most observers thought that the technology was intriguing, but the costs and degree of difficulty were both very, very high. At that stage, fixed-bottom offshore was installing only a few hundred megawatts per year, costs were high and going up, and the future of the sector appeared in doubt. How things have changed!By Steve Sawyer, Secretary General, Global Wind Energy Council

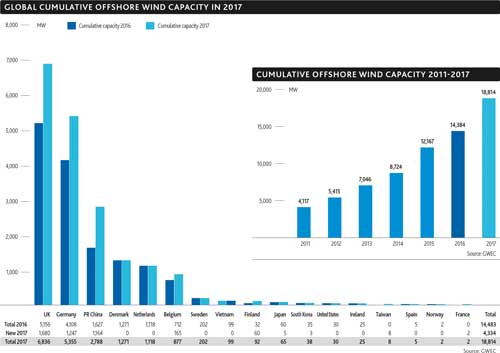

As outlined in our annual Global Wind Report released in late April, of the 539,123MW global wind power capacity as of the end of 2017, 18,814MW is offshore, or about 3.5%. However, of the 52,492MW newly installed in 2017, 4,334MW is offshore, or about 8.3%. For the European Union, offshore made up about 20% of the 2017 market. Offshore wind installed in the next five years will have a levelised cost of electricity of half that installed in the last five years. The low prices in recent tenders have sparked global interest and offshore is now spreading across the globe, with new markets in Asia, North America, Australia and even Brazil.

Of the 18,814MW of global offshore wind as of the end of 2017, only about 50MW is floating: one commercial project off Scotland of 30MW and most of the rest in various demonstration projects in Japan. So why all the excitement about floating technology?

- The potential for offshore in new markets in places without a broad shallow continental shelf, in particular off Japan, the west coast of the USA, the Atlantic coast of Europe (France, Portugal and Spain) and numerous other locations.

- The opportunity to place turbines where the best wind resources are rather than being constrained by water depth and bottom topography, thus increasing yields and improving the economics.

- The opportunity for mass production of foundation components. There are too many different designs at present, but there is a huge amount of research going on and once the industry has settled on one or two basic designs, mass production can reduce costs.

- There is still enormous potential for cost reductions in the sector, with the very real possibility of getting to lower prices than fixed-bottom systems, especially as more and more of the shallow-water nearshore locations are taken up.

Until recently, the prohibitive cost has stood in the way of raising the capital to deploy more and more demonstration projects and small commercial projects so that the technology can mature. However, buoyed by the unexpectedly rapid cost reductions in the fixed-bottom offshore sector, that money seems to be flowing at the moment, both from governments and from major players in the marine engineering sector, whose expertise is invaluable. We will see hundreds of megawatts of deployment over the next several years: on spar buoys, on all manner of semi-submersible platforms, and on a variety of other more experimental platforms. The next challenge will be to find the capital for the rapid buildout of the technology once the market decides on a small number of ‘mainstream’ designs. It will not happen overnight but by the end of the next decade I am sure that we will start to see the percentage of floating offshore rising rapidly in the global wind power mix, as its fixed-bottom counterpart is today.

Until recently, the prohibitive cost has stood in the way of raising the capital to deploy more and more demonstration projects and small commercial projects so that the technology can mature. However, buoyed by the unexpectedly rapid cost reductions in the fixed-bottom offshore sector, that money seems to be flowing at the moment, both from governments and from major players in the marine engineering sector, whose expertise is invaluable. We will see hundreds of megawatts of deployment over the next several years: on spar buoys, on all manner of semi-submersible platforms, and on a variety of other more experimental platforms. The next challenge will be to find the capital for the rapid buildout of the technology once the market decides on a small number of ‘mainstream’ designs. It will not happen overnight but by the end of the next decade I am sure that we will start to see the percentage of floating offshore rising rapidly in the global wind power mix, as its fixed-bottom counterpart is today.Biography

Steve Sawyer joined the Global Wind Energy Council as its first Secretary General in April 2007. Mr Sawyer has worked in the energy and environment field since 1978, with a particular focus on climate change and renewable energy since 1988. Steve is also a founding member of both the REN21 Renewable Energy Policy Network and the International Energy Agency’s Renewable Industry Advisory Board.

Steve Sawyer joined the Global Wind Energy Council as its first Secretary General in April 2007. Mr Sawyer has worked in the energy and environment field since 1978, with a particular focus on climate change and renewable energy since 1988. Steve is also a founding member of both the REN21 Renewable Energy Policy Network and the International Energy Agency’s Renewable Industry Advisory Board.